canadian Tenants may be Liable to Pay their Landlord’s Income Tax Bills if the landlord lives abroad25/4/2024  4175 Sainte Catherine West in Westmount, Quebec. David lived on the 5th floor. David rents a fifth floor apartment in Westmount, Montreal. He likes it so much he stays there for 20 years. Two years after he leaves, David receives a disconcerting letter from the CRA. It claims he must pay tens of thousands of taxes owed by his landlord. David is incredulous. Clearly a mistake has been made. It shouldn’t take long to fix. But the CRA stands firm. David sues. He loses. David lodges an appeal. That appeal works its way through the legal serpentine and lands in Canada’s Tax Court. The outcome? David loses again, once and for all, and is ordered to pay his landlord’s tax bill of $43,650 + interest + a penalty + court costs. This is a true story. It played out for years and concluded in 2023 in Canada's Tax Court as:  David’s landlord Sebastiana lives in Italy. She owns the Montreal apartment as an investment, but is not a Canadian resident. Canada’s Income Tax Act has a provision that imposes a 25% tax on certain income a non-resident receives from a Canadian resident, including rental income. Under this rule, Sebastiana should have paid 25% of her gross rental income to the CRA. But she didn’t. The government knows it’s hard to track down people abroad. To ensure compliance, the Income Tax Act also contains a provision that says this 25% tax can be claimed from the Canadian resident who made the payment, which the CRA did. In plain text, any tenant whose landlord lives abroad could be liable to pay 25% of their gross rent costs to the CRA, even if they have no clue where their landlord actually lives. The burden of knowing the residency background of the landlord is placed on the tenant. The tenant must then ascertain that the landlord will not be paying the 25% withholding tax, and respond by withholding 25% of their monthly rent and remitting this to the CRA. Crazy stuff, but all legally defensible because it’s written in Canada’s tax statutes. The Details of David vs. SebastianaThe apartment was originally owned by Anjar Investments Ltd. Sebastiana was one of three Anjar shareholders, all of whom shared the same last name. It appears this was a family-run holding company. Anjar sold the apartment to Sebastiana in 2006. It appears that Anjar was paying the 25% withholding tax until the 2006 sale, and Sebastiana continued paying it for four years after the transaction (until 2010). Because David began living in the apartment in May 1996, but the CRA only claimed unpaid tax for the years 2011 to 2016. David signed a new three-year lease in May 2010 with Sebastiana as the lessor. Sebastiana countersigned from Italy, but listed a Quebec mailing address on the document. The lease also contained two phone numbers, one in Montreal and the other an international number. Her email address ended in .it (for Italy). David met Sebastiana on three occasions: in 2010 when she delivered the lease, in 2014 or 2015, and once in 2017. David is a small business owner and began paying his rent through his numbered company in 2011, so it’s his company that is officially on the hook for the tax bill. He says he was never told that his landlord lived in Italy. How to win the Case As worrying as this case is, David could not win his appeal by claiming it was unfair of the CRA to make him pay his landlord’s debt. Part XIII, section 250 of the Income Tax Act is unequivocal on this. His only chance was proving that Sebastiana was not living in Italy, but actually a Canadian resident.

His evidence was weak, though. All he had was the old Anjar business registration that showed Sebastiana as a shareholder of the family company, a social insurance number, and a TD Bank Trust account where he deposited his rent. The SIN was proof that Sebastiana had at one time lived in Canada, but it did not prove she hadn't left. And so, David lost his appeal. He must pay his landlord’s tax bill. It’s a grossly unfair outcome. How can a tenant be expected to background check their landlord to learn if they are living abroad? And how could they ever know if their foreign-based landlord is paying their Canadian tax bill? You sign a lease, you pay your rent, end of story. But not in Canada.

0 Comments

This video belongs to KenMcElroy - so please visit his YouTube channel - but it is such a good 101 primer on real estate investing, it deserves a repeat here. Ken markets this video as how to make money in real estate in 2024 and 2025 because of an expected liquidation of multifamily properties by owners who can't afford their interest payments.

But it's really a basic illustration of how to buy real estate successfully. 1. Buy low. In this case Ken says lots of distressed properties will hit the U.S. market in the next 24 months as high interest rates bite. Same goes for Canada. Owners will be forced to sell - or go bankrupt. People bought properties at large premiums during the COVID go-go years when governments were shovelling stimulus money out the door, artificially juicing every kind of market: cars, hard goods, housing, electronics, shipping, labour, construction supplies. Real estate looked like a great bet. Prices were flying, but loans from banks were available for next to nothing, so real estate still seemed 'cheap'. Real estate is a great store of value. But overpaying - for anything - is how you lose money, not make it, because loans must ALWAYS be paid back. 2. Make sure your income exceeds your expenses: Sounds pretty basic, right? Create positive cash flow on your buy-and-hold real estate by getting more rent than you spend on the loan, insurance, utilities, and so on. BUT...when planning an investment property purchase, net cash flow calculations also require a set of what-if scenarios in the form of a sensitivity analysis. A sensitivity analysis creates new financial models in the event X happens. In this case, X is higher interest rates. For example, when modelling out the purchase of a new property in Excel, create five columns with a range of interest rates from best to worst in them, and model out future returns. If you don't build in margins of safety in the event of interest rate increases, you are exposing yourself to errors through ignorance. We all knew interest rates could not stay near zero. We all knew inflation would rise - at least anyone with business sense and a basic understanding of economics did. The law of supply and demand may get suspended during bouts of irrational market exuberance, but foundational market principles never go away. Effectively managed markets always self-correct. Prices rebalance themselves, cheap cash goes away as banks tighten their loan books, and for those still able to refinance, the cost of money rises. Those who bought property wisely will get bruised, but they will survive. Those who didn't include X in their planning will get burned. Then, those with cash who were waiting patiently on the sidelines for naive/inept investors to self-immolate, will scoop up all the discarded housing that the burned investors are forced to sell at bargain basement prices. Such is capitalism.

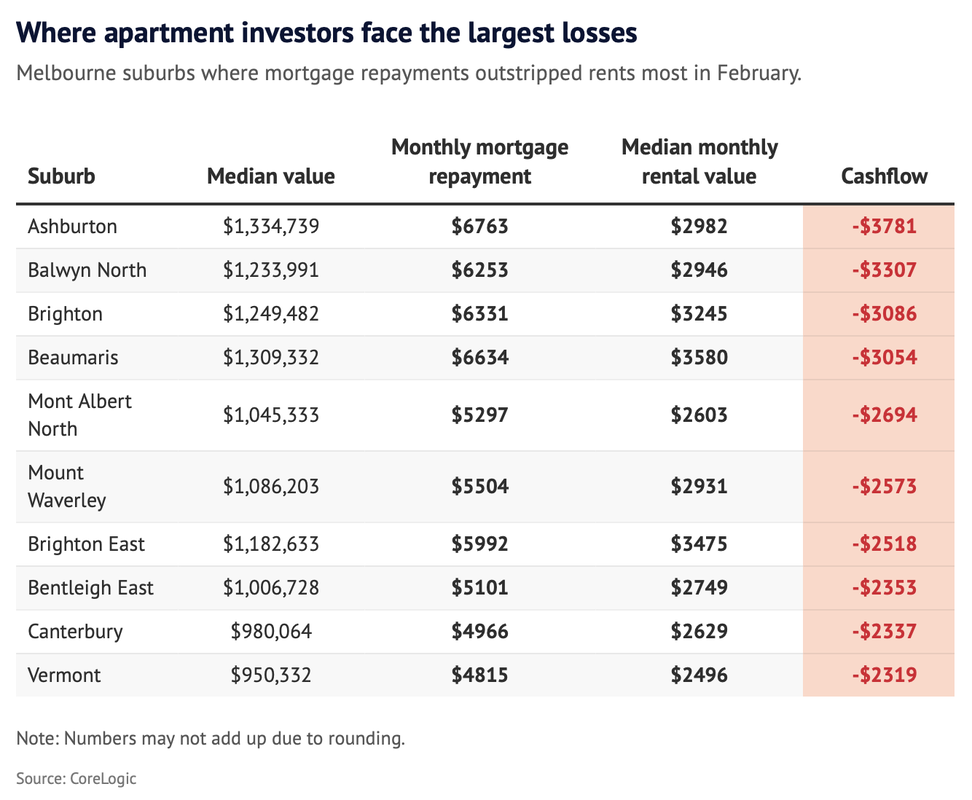

That man, Ramone Simone, became her paramour and business partner. He convinced her to leave her family, home, and her job at the Fort Lee Diner, recommending she head to New York City. He paid for her to stay for one week at the Barbizon Hotel for Women, which was the only hotel left in New York City at the time that rented rooms only to women.  Upon leaving home at the behest of an older man and heading for the bright lights of Manhattan, Barbara’s mother accused her of being a prostitute. Simone did give Corcoran $100 to buy her first NY outfit, but she says that’s where the cash gifts ended. So convinced was Simone of Corcoran’s skills, he gave her $1,000 to start a company. Simone kept a majority stake of 51% and Corcoran owned the remaining 49%. It was a fine investment, because that $1,000 helped her begin a residential realty in New York. She started by renting out apartments all over the NYC, hustling against the male competition and whipping them with her wiles, passion, and never-say-die attitude. She ran her first apartment-rental business out of her apartment on East 86th Street, which she shared with two roommates. He company, The Corcoran Group, is now worth more than $5 billion. Corcoran was hungry. She ground her way to the top and even took on Donald Trump in the 1990’s when he stiffed her on a large invoice. Peek Inside Barbara Corcoran's New York ApartmentBarbara’s first commission check was $340, which she spent on a new coat. She had a bouncy, playful personality that made her stand out in a very male industry. On one occasion, she was contacted out of the blue by a wealthy patron who sent her an endless stream of young Citibank recruits, all of ehom needed a home in New York. It was such easy money, Corcoran described it as like flipping pancakes. The number of young men parading in and out of her apartment was not lost on the building’s super though, who reported her to the building’s owner for being a prostitute. The super even stuck a bright red notice on her door: Eviction Notice for Prostitution. Embarrassed, Corcoran had to once again deny she was a prostitute. But she was such a sales hot-rod, not only did she convince the building’s owner she wasn’t a hooker, she turned the office visit into a marketing pitch convincing him to make her his exclusive listing agent. Instead of being evicted, she signed up to show all his vacant apartments, ironically boosting the number of young men visiting her home/office. Barbara Corcoran the Exceptional Self-Marketer Barbara Corcoran is dynamite when it comes to marketing and self-promotion. When hiring new sales agents, she never wrote boring ads like, “Position Open, salespeople wanted. Make high commissions”. Instead, she wrote, “One Empty Desk” in a double-sized heading. “Join a company that’s a lot of fun, cleaning up and having a blast.” And as for being a woman in a very male and very sexist New York City real estate industry? “[Being a woman…] was an advantage. It was an advantage, because I could then walk into the rooms and I always wore short, red skirts with my jackets, and I had great legs, and I knew it. And everybody would turn to look at — because a girl stood out. You didn’t even have to be special. You just had to be a girl, and you were different. “But as competing with them, I never saw myself as a woman. I never saw it as a disadvantage or a real advantage. I saw myself as a competitor, just a competitor. And boy, if they treated me badly, or spoke down to me, or didn’t give me any credence that I could possibly make it in their world — they thought I was a passerby. I would say to myself, “You just wait, I’m going to become your biggest rival.” Overcoming Dyslexia Barbara Corcoran is dyslexic. She was bullied at school for this and always felt stigmatized and ‘less-than’ because of it. School was an unpleasant chore. As a business woman, she overcame her dyslexia through clever workarounds. The files in her office were organized by colour instead of having written labels. One bedroom apartments were given one colour and two bedroom ones a different colour, and so on. She structured her business visually. When sending thank you notes, instead of writing, she pasted together images to express herself. Colour-coding and photos were just one of many systems she put in place to scale her business. On a single day in the late 1970’s, Corcoran made a cool $1.225 million USD. And she did this at a time when interest rates were 18% and no one was buying real estate. New York City’s real estate market was dead! The kicker is that she made that money in only three and a half hours selling apartments that were acknowledged as duds – apartments that the owners had given up on because no other realtor could sell them, they were that bad: no views, no kitchens, back walls, different locations across the city. Awful! So, what did she do? Corcoran leveraged the scarcity heuristic. When people think the supply of something is running low, they are deeply psychologically motivated to buy some of that thing before it is gone forever. This was the plan: all 88 dud apartments were priced exactly the same: $59,900. Corcoran told her realty sales agents they could notify only their best two customers of the sale. No more! This was an exclusive offering. She had 300 sales people so that generated 150 leads. Corcoran leased a bus, decked it out with signs that said Wheels and Deels, and drove the buyers to all of her locations. At each stop, she had a stack of sales contract, each one with her signature on it, giving the impression that these were for completed sales. More scarcity. It worked. Buyers were lined up out the door. Every dud unit sold, and Corcoran earned $1.225 million in three and a half hours. She never advertised during her early career. All her listings and business success came via word of mouth. Showing off her Pacific Palisades Double-Wide Trailer Park Home which is where she stays when in Los AngelesFighting Donald Trump in Court & Winning In 1994, Barbara Corcoran took on Donald Trump because Trump had failed to pay her millions of dollars in owed commissions. Looking back, Corcoran describes Trump as, “an intimidating man, a real-life bully in every way.” And that’s what made her take him on. “I’m not a fighter… I don’t like to fight. I’ll walk a mile to avoid a fight. But when someone insults me, it brings out the fight in me. I don’t know where that comes from. “It was the first year I made a real profit in Corcoran Group, because I never made money, because I was always throwing my money back in and living so cheap so that I could afford to open offices. Always, the money went to the business, the money went to the business, never came to me. And that year, I had more money than I could spend. I had over a million dollars in profit. The year before, the many years before that I either had losses, or 100,000, but it cost me $500,000 to sue. But I had the cash, think about that. So, I felt powerful, and I got the money to fight it, and I’m certainly not going to walk away. Because you know what my thinking is? I’m walking away from a well-fought fight. You resent it and regret it for the rest of your life. I didn’t want to be that girl who said, “Son of a bitch, how did he get away with…” You really, you regret when you don’t confront things, I think in anything, but particularly with a moral fight. And in my mind, that was morals, it’s all about morals. I earned the money, “You signed you’d give it to me and you’re not giving it to me? You’re suing me instead? Oh, no, I don’t think so.” Corcoran won the case, but it took her five years to get the money. Trump was close to bankruptcy at the time, so the judged ordered him to pay $55,555 a month for five years. After accepting the first instalment in a hand-delivered check, Corcoran told the messenger to wait a moment. She dashed inside and hand wrote a note that said, “Thank you Donald. I really appreciate the check.” In return, Trump scrawled on the note card in thick marker “Rejected” and sent the flowers back to Corcoran. So, each time Corcoran received a Trump check over the next five years, she bought herself a bouquet of flowers – choosing blooms that she personally loved - and sent them to Donald Trump, knowing that he would send them back and she would get a lovely bunch of flowers for her home or office. The quotations in this blog post were taken directly from Barbara Corcoran’s interview with Tim Ferris. A copy of this interview is included below. Please watch it and support Tim Ferris’s eponymous podcast. It is brilliant!  Did you know that in Australia you buy residential homes via auction, not through competing back and forth offers via realtors? People stand on the street in front of the house for sale, an auctioneer kicks things off, and people in the crowd call out bids. Just like on Storage Wars. https://www.abc.net.au/news/2023-07-08/property-prices-auction-sales-australia-melbourne-sydney/102549152 Did you also know that Australia is one of the least affordable places to own a home? Melbourne, a major city of five million people, is similar to Vancouver in terms of the tremendous demand for homes and rentals, but a limited housing supply. There is one major difference between the Canadian and Australian housing markets, though. In Australia, investors can offset negative cash flow on an investment property. If your property’s expenses are greater than your rent, the negative balance can be claimed as a deduction on your personal tax return. This is called negative gearing and is perfectly legal. In fact, it’s a real estate investing strategy. Negative gearing is especially appealing for people with high personal incomes. They can deliberately buy investment properties which lose money, creating negative cash flow from day one, and then make profits on the back end by claiming that loss on their personal tax return. Some investors are losing thousands each month. More than $40,000 per year. And yes, these suburbs are nice places to live. But they're not Bel Air, wealthy, mansion territory. We're talking leafy bungalow- lined streets I’m unsure of the rationale behind this policy, because to me it seems like a surefire way to overheat the property market because prices will be pushed ever higher. There are no consequences for buying a bad asset and overpaying. Negative gearing is not new tax policy, and the Australian government must have it reasons for allowing it, but perhaps it’s also playing a role in the country’s out of control real estate prices because it encourages speculation. The one negative consequence for investors is that they still need to cover their mortgage payments each month which can sometimes be thousands of dollars less than their rental income. But I guess if your personal income is large enough, offsetting such large losses must still work for them . As an example, the chart below shows suburbs in Melbourne where investors are bleeding cash i.e. have seriously negative monthly cash flow, but the owners don’t sell because they must have high personal incomes and the tax offset makes it worthwhile to hang on. In situations like this, the only profits investors can make is through capital gains.  Please contact me if you would like to invest in our Ontario, Canada campground program that leases waterfront lots and places tiny homes on them for Retirees, Down-Sizers and Digital NomadsI like small footprint homes. Not to live in, per se. I have a normal-sized home for that. Instead, my business partners and I buy campgrounds in central and eastern Canada and then offer tiny homes to buyers who want to make our campgrounds their full-time home. Here’s how it works:

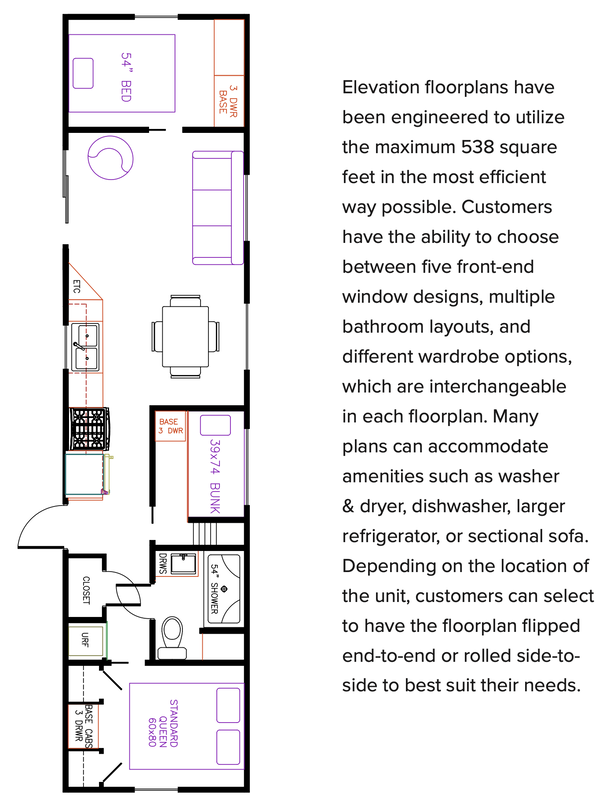

All of our small footprint homes will blow your mind away when you see what 538 square feet of floor space can become: KITCHENS       LIVING SPACES      BEDROOMS

BATHROOMS

UTILITY SPACES

EXTERIOR  Paying tenants to vacate a property that we as landlords want to renovate is standard practice. The building will get spruced up – sometimes gutted and rebuilt – and the tenants have an incentive to move on. That’s fine until you have a rental market like we have right now in Canada’s major cities. Vancouver has a vacancy rate of .9% and the Greater Toronto Area is not much better. There just aren’t any new homes for tenants to move to at comparable rates. If a tenant has lived in a building for many years, their current rent could be as much as 50% or 60% lower than the going rate. And tenants who have stayed put in one rental for that length of time are likely to be vulnerable members of society: elderly, infirm, working poor families. It doesn't feel good to move along people in need, so the right thing to do is hire a realtor who can find these tenants a new home. Unfortunately, since Canada has so little housing for its growing population, any replacement accommodation is guaranteed to cost more than what these displaced tenants can afford. I don't have any solutions to this issue – if I did, I’d be in politics. What disturbs me however is how some ill-intentioned people use tenant protection laws to game unsuspecting landlords. They move from building to building, fail to pay rent, and run out the clock on the eviction process. They know that the long, bureaucratic eviction process and the giant backlog some municipalities have before cases are heard, protects them for months, even years. They might even trash the place before they move to the next rental they plan to squat in, and start the whole extortion scheme all over again. It’s extortion, because these professional squatters are protected by the law and demand large sums of cash from property owners to leave. Real estate investors are viewed as rich, landed gentry who deserve to be taken advantage of – even if they are just mom and pop investors, trying to make a go of things. The story below was compiled by CBC TVs investigative unit and is worth viewing. The story’s intro is as follows: Some small landlords say they're facing outrageous demands from tenants to hand back the keys. CBC's Ioanna Roumeliotis breaks down what’s behind the rise in "cash for keys" deals and why advocates say it's time tenants got the upper hand. PLEASE SUPPORT LOCAL JOURNALISM, INCLUDING THE CBC I’m positive you've never read before this book before, but you should. Here is the opening paragraph:

The book is The Dhando Investor: The low-risk Value Method to High Returns by Moohnish Pabrai, John Wiley & Sons Inc, 2007  All credit for the ideas in this post goes to the author Moohnish Pabrai. I’ll limit this post to talking about chapter five, The Dhando Framework. Even though I want you to read the actual book, I’m not giving much away by revealing the following nine points. I’ll even add one of my own to round them out for an even ten. Please note, the nine points below are taken directly from the book but the explanations provided are really adaptations because they were created by me to make the Dhando Framework more directly applicable to real estate investing. 1. Invest in existing businesses.Pabrai says it’s much less risky to buy an existing business with a well-defined business model than doing a startup. My thoughts: True. But this all depends on how you view risk. Most people see risk as something to be avoided because it represents pain, suffering and financial loss. I view risk as an opportunity. It involves an ill-defined problem that I need to think through. I allocate percentages to my chances of success and failure. There is often safety in sticking with the tried and tested, but it is on the frontier of the unknown that immense success and financial reward can be found. But remember: risk is double-edged. The line between great profit and life-altering failure is thin. Do you have the emotional and financial resilience to bounce back if your analysis is wrong or an unexpected event wipes you out? That’s a question between you, your mirror, and your life partner. 2. Invest in simple businesses. Pabrai advises buying simple businesses which experience ultra-slow, long-term change. He cites the Patel’s purchase of roadside motels as an ideal example. Computers have made the travel industry more IT-centric, but motels/hotels are at their core still a basic service business. As long as humans travel long distances, they will always need a place to sleep and refresh themselves. The fundamental economics of the business and the basics of good service are universal and unchanging. My thoughts: True. Air BnB and VRBO are simply new spin on an old problem. They monetize latent supplies of accommodation that no-one even knew existed: empty bedrooms in people’s homes. At the end of the day, a nice room in a nice hotel with nice amenities is all most people desire. 3. Invest in distressed businesses in distressed industries. Pabrai says, “the very best time to buy a business is when its near-term future prospects are murky and the business is hated and unloved. In such circumstances, the odds are high that an investor can pick up assets at steep discounts to their underlying value.” He uses Lakshmi Mittal, the Indian entrepreneur, as an example. Lakshmi built a global steel manufacturing empire by buying unwanted steel mills around the world when the steel prices were in the doldrums and the mills were being got rid of at fire sale prices. My thoughts: There are many ways to make money on a real estate deal. The first one is your purchase price. If your entry strategy is lousy and you pay too much, it doesn't really what your exit strategy is; you’ll still lose. Or as Warren Buffett wrote, “Never count on making a good sale. Have the purchase price be so attractive that even a mediocre sale gives good results.” 4. Invest in businesses with durable competitive advantage – a moat to keep away the competition. Pabrai leans on Warren Buffet completely for this one. He even quotes him: “The key to investing is not assessing how much an industry is going to affect society, or how much it will grow, but rather determining the competitive advantage of any given company and, above all, the durability of that advantage. The products and services that have wide, sustainable moats around them are the ones that deliver rewards to investors. I don’t want an easy business for competitors. I want a business with a moat around it. I want a very valuable castle in the middle and then I want the duke who is in charge of that castle to be very honest and hardworking and able. Then I want a moat around that castle. The moat can be various things: The moat around our auto insurance business, GEICO, is low cost” My thoughts: Nothing to add. 5. Few bets, big bets, and infrequent bets. Pabrai says Dhando is about taking low risk, high return bets. Dhandho (pronounced dhun-doe) is a Gujarati word. Dhan comes from the Sanskrit root word Dhana meaning wealth. Dhan-dho, literally translated, means, “endeavors that create wealth.” The street translation of Dhandho is simply “business.” What is business if not an endeavor to create wealth? However, if we examine the low-risk, high-return approachto business taken by the Patels, Dhandho takes on a much narrower meaning. We have all been taught that earning high rates of return requires taking on greater risks. Dhandho flips this concept around. Dhandho is all about the minimization of risk while maximizing the reward. The stereotypical Patel naturally approaches all business endeavors with this deeply ingrained riskless Dhandho framework - for him it’s like breathing. Dhandho is thus best described as endeavors that create wealth while taking virtually no risk.” Pabrai uses the example of Papa Patel to explain: “It is 1973. Papa Patel has been kicked out of Kampala, Uganda, and has landed as refugee in Anywheretown, USA, with his wife and three teenage kids. He has had about two months to plan his exit and has converted asmuch of his assets as he could into gold and other currencies and has smuggled it out of the country. It isn’t much—a few thousand dollars. With a family to feed, he is quickly trying to become oriented to his alien surroundings. He figures out that the best he can do with his strange accent and broken-English speaking skills will be a job bagging groceries at minimum wage. "apa Patel sees this small 20-room motel on sale at what appears to be a very cheap price and starts thinking. If he buys it, the motivated seller or a bank will likely finance 80 percent to 90 percent of the purchase price. His family can live there as well, and their rent will go to zero. His cash requirement to buy the place is a few thousand dollars. Between himself and his close relatives, he raises about $5,000 in cash and buys the motel. A neighborhood bank and the seller agree to carry notes with the collateral being a lien on the motel. As one of the first Patels in the United States, Dahyabhai Patel succinctly put it, “It required only a small investment and it solved my accommodation problem because [my family and] I could live and work there.” Papa Patel figures the family can live in a couple of rooms, so they have no rent or mortgage to pay and minimal need for a car. Even the smallest motel needs a 24-hour front desk and someone to clean the rooms and do the laundry— at least four people working eight hours each. Papa Patel lets all the hired help go. Mama and Papa Patel work long hours on the various motel chores, and the kids help out during the evenings, weekends, and holidays. Dahyabhai Patel, reflecting on the modus operandi during the early days, said, “I was my own front-desk clerk, my own carpenter, my own plumber, maid, electrician, washerman, and what not.” With no hired help and a very tight rein on expenses, Papa Patel’s motel has the lowest operating cost of any motel in the vicinity. He can offer the lowest nightly rate and still maintain the same (or higher) profitability per room than his predecessor and competitors. As a result, he has higher occupancy and is making super-normal profits. His competitors start seeing occupancy drop off and experience severe pressure on rates. Their cost structures prohibit them from matching the rates offered by the Patel Motel - leading to a spiraling reduction in occupancy and profits.” p. 6-7 My thoughts: Place the odds in your favour and you are sure to win over the long term. The hard part? Being patient. Waiting until you find investments that offer you great odds. Papa Patel is a classic story of the tools we still use to create wealth through real estate: house hack (live in your investment property while also renting out part of it; managing the property yourself. Use family values to offer a clean establishment with attentive service. Outmuscle the competition by maintaining standards high and expenses low so that rental prices are always competitive. Succeed at all these things and you will create strong cash flow that will provide a good living and help you accumulate savings large enough for a down payment on a new property. So, the hotel/real estate growth cycle goes, slowly, on and on.  Part 2 of this post will include the remaining four recommendations made by Moohnish Pabrai (seen above) plus one of my own.

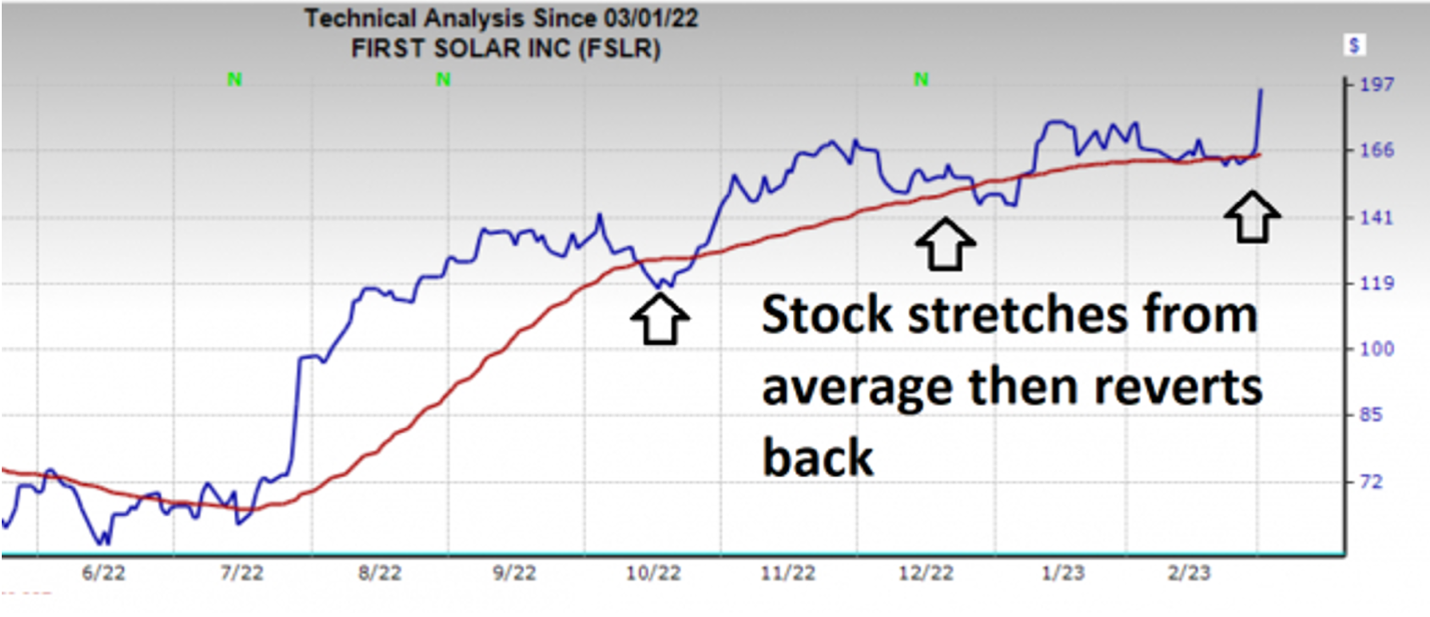

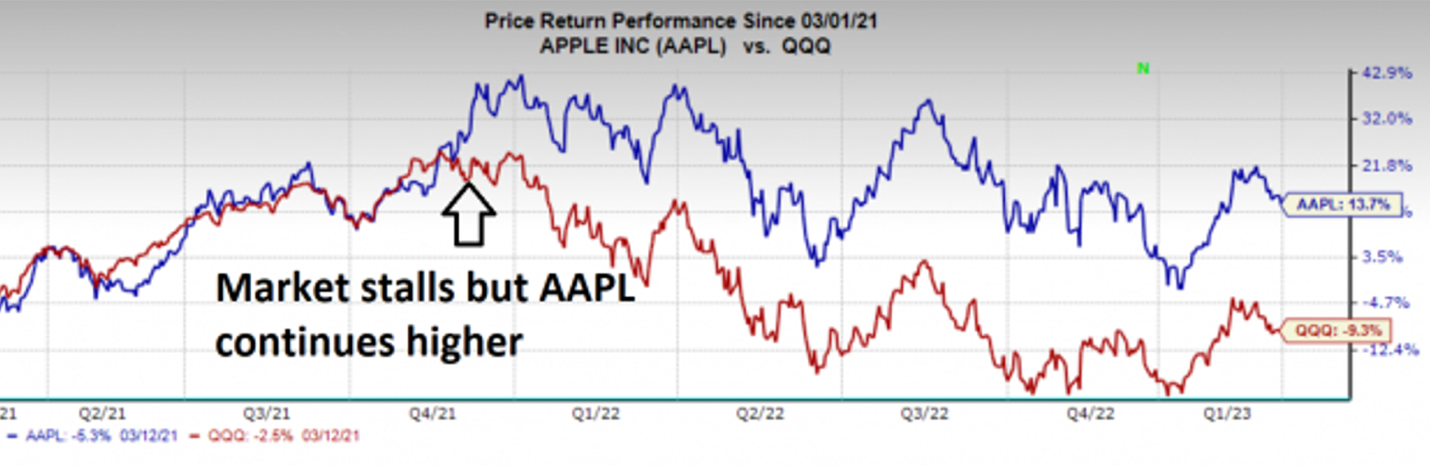

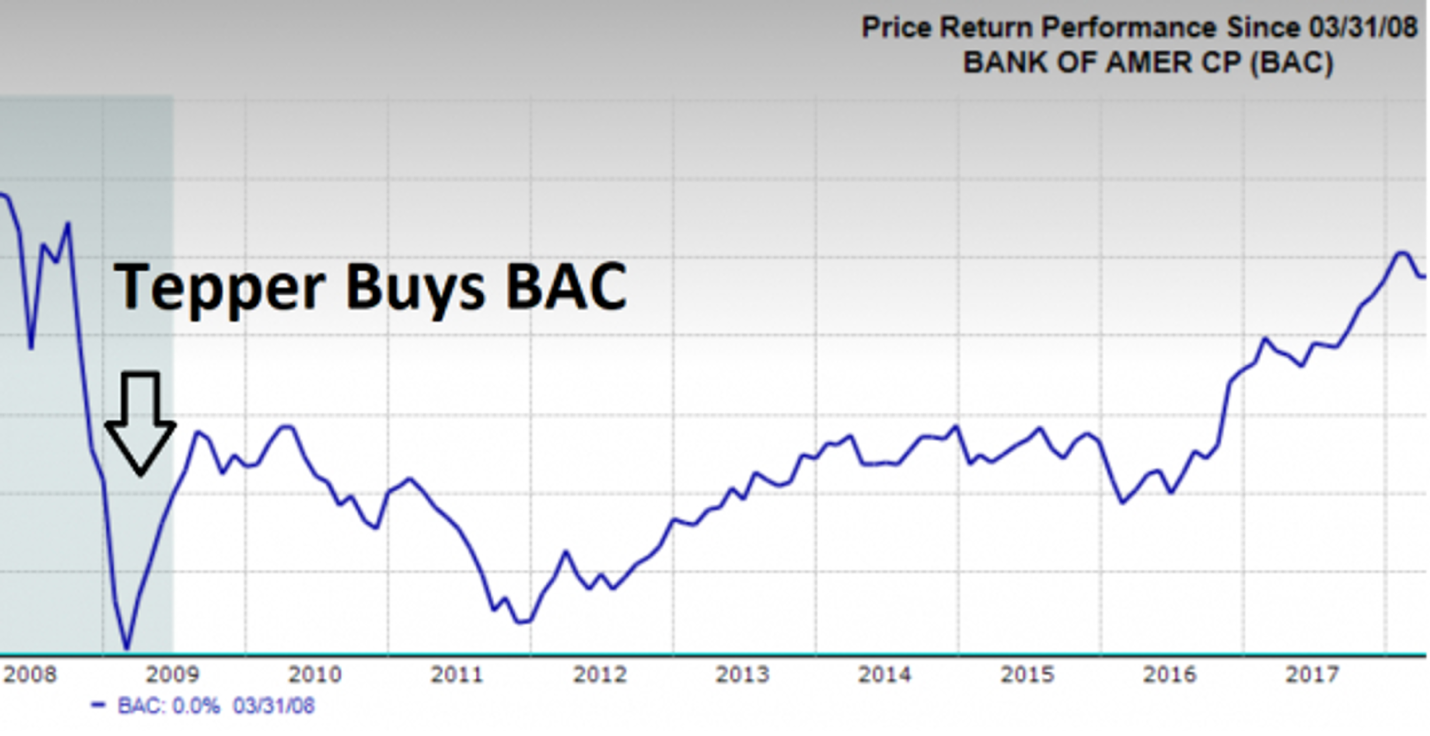

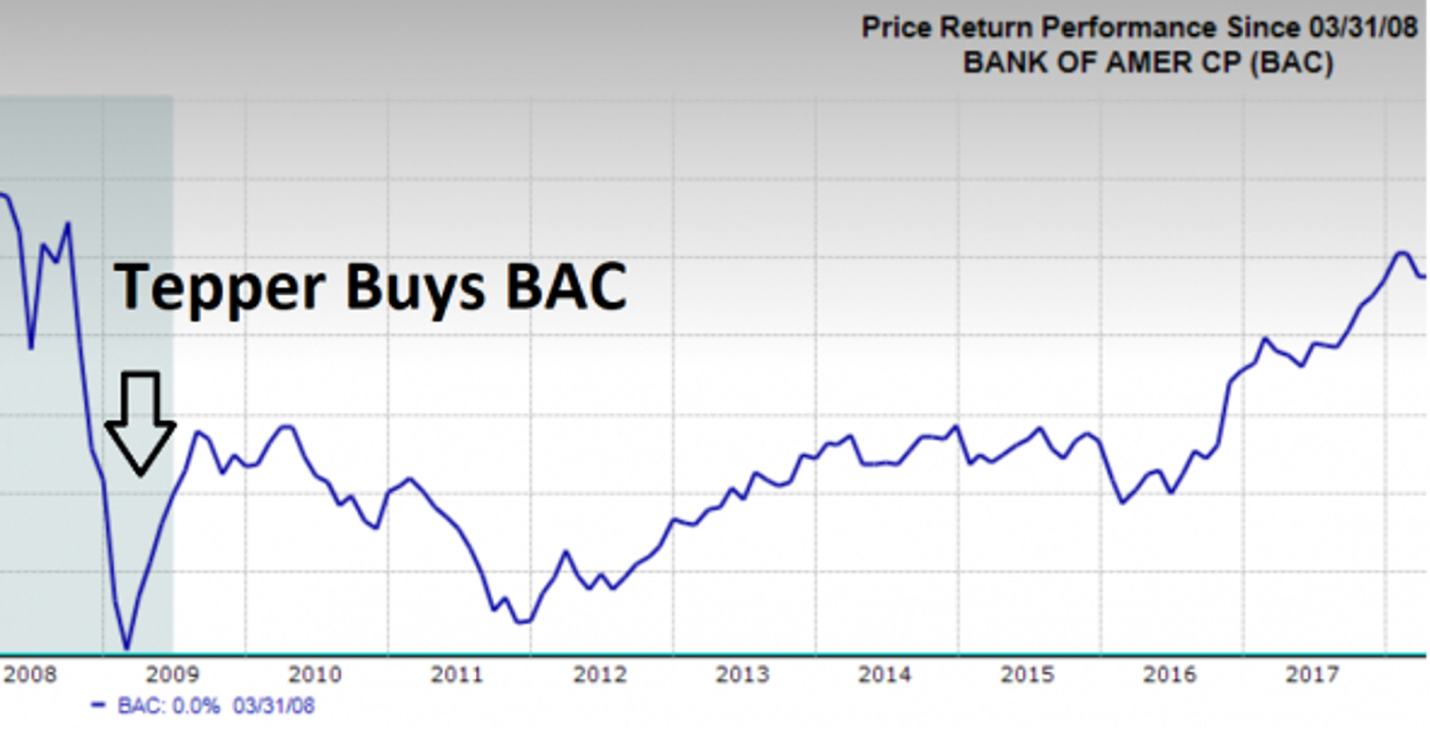

Fact 1: The S&P500 rose more than 24% in December 2023. It is only 1% away from hitting its all-time historic high. The S&P500 has ended positive for the last nine consecutive weeks. That kind of winning streak hasn’t happened since 2004. Fact 2: $69 billion of investor cash flowed into ETFs in December. That’s the highest inflow of cash for two years, since just before the stock market’s all-time peak. Fact 3: The NASDAQ is almost 8% above its 50-day moving average. Fact 4: U.S. small cap stocks have also been swept up in the Santa rally. The Russell 2000 index sprang upwards by more than 3.7% in the last two weeks of December. Fact 5: Almost 90% of S&P stocks are now priced above their 50-day moving average. 75% are above their 200-day moving average. These facts indicate that the U.S. market is significantly overbought (priced too high). It appears that investors have accepted the idea that the U.S. will experience a ‘soft landing’ for its economy after so much inflationary spending during the COVID pandemic. I have some thoughts on this but they are just a prediction, so I’ll keep them to myself. All I’ll say is remember Bob Farrell’s rule number #5: The public buys the most at the top and the least at the bottom. If you’re unaware of who Bob Farrell is, below is an article published on the nasdaq.com website. To be clear, the article below is not my work, but I recommend it. Wall Street Legend Bob Farrell's 10 Rules https://www.nasdaq.com/articles/wall-street-legend-bob-farrells-10-rules Who is Bob Farrell? Twelve years after the conclusion of the Second World War, Bob Farrell started his career at Merrill Lynch as a technical analyst. Before kickstarting his illustrious career at Merrill Lynch, Farrell studied at the prestigious Columbia business school under Benjamin Graham and David Dodd. Graham and Dodd are widely hailed as the “godfathers of modern value investing” and are best known for their best-selling book “Security Analysis,” which was first published in 1934. In fact, Graham and Dodd are so synonymous with value investing that Warren Buffett (also a student of Graham at Columbia) attributes much of his success to the classic work and teachings of the two value investing legends. A Wall Street Pioneer While Mr. Farrell was educated under the value investing umbrella, he found his niche and success on Wall Street at the intersection of technical analysis, sentiment, and market psychology. Though this type of analysis was considered unconventional and even frowned upon at the onset of his career, by the end of Farrell’s nearly five-decade run on Wall Street, it had become mainstream. Farrell became so respected in market circles that his daily newsletter was read by several of the world’s sharpest money managers, including the likes of multi-billionaire George Soros. There is little Mr. Farrell hasn’t seen or experienced throughout his career. Below are Farrell’s 10 Rules: 1. Markets tend to revert to the mean over time. Like a rubber band stretched in one direction, markets tend to snap back to the other direction eventually.  Image Source: Zacks Investment Research 2. Excesses in one direction will lead to an opposite excess in the other direction. Think about the internet boom and bust. At one point, stocks like Pets.com would rocket 200% in a single trading session just because they had “.com” in the name. During 2000-2003, the market unraveled just as violently in the opposite direction. The COVID-19 crash and subsequent rally afterward is another prime example:  Image Source: Zacks Investment Research 3. There are no new eras – excesses are never permanent. History is littered with boom-and-bust periods – nothing lasts forever. The great “Tulip Mania” of the 17thcentury, the dot com bust of 2000, and the 2008 housing debacle personify this rule. 4. Exponential rapidly rising or falling markets usually go further than you think, but they do not correct by going sideways. The meme craze that occurred a few years ago is a good illustration of this rule. In 2020, GameStop GME ran from $1 to $5.50 in five months. After more than a 500% move in such a short time, that wasn’t the end. The following month, shares soared 1600% to $120 a share before correcting to their current price of $18 per share.  Image Source: Zacks Investment Research 5. The public buys the most at the top and the least at the bottom. Most investors let their emotions get the best of them. Generally, if the public invested when they were most fearful and sold when they were most giddy, they would be much more profitable. In late 2022, most sentiment gauges showed fear. Over the next few months, the market went on a tear. 6. Fear and greed are stronger than long-term resolve. The fast-moving pace of Wall Street can wreak havoc on investor emotions. When the opening bell rings and real money is on the line, it is akin to having a volume dial on emotions for most investors. The lack of discipline to create and stick to a well thought out investing plan can be detrimental to investors. Even if a well-thought-out plan is created, execution always supersedes intentions. 7. Markets are strongest when they are broad and weakest when they narrow to a handful of blue-chip names. A “blue chip” is a well-established mega-cap company such as Apple AAPL. Breadth refers to the number of stocks participating in a rally. The participation gauge is an important measure to follow because it can provide clues to a market breakdown prior to it occurring. In early 2021, Apple and other mega-cap blue chip stocks continued higher as the market began to stall slightly – a subtle, early caution flag for savvy investors who were paying attention.  Image Source: Zacks Investment Research 8. Bear markets have three stages – sharp down, reflexive rebound, and a drawn-out fundamental downtrend. Because the public typically buys the dip at the wrong time or shorts “in the hole” when stocks have already moved down rapidly, equity markets usually have a violent “bear market rally” before trending lower.   Image Source: Zacks Investment Research 9. When all the experts and forecasts agree – something else is going to happen. Contrarian, independent thinking is the clearest path to success on Wall Street. Following the Global Financial Crisis, David Tepper bought Bank of America BAC in 2009. Later when he recounted the trade, he said, “I felt like I was alone”. The trade ended up netting him $4 billion. To achieve outstanding results, you must think differently.  Image Source: Zacks Investment Research

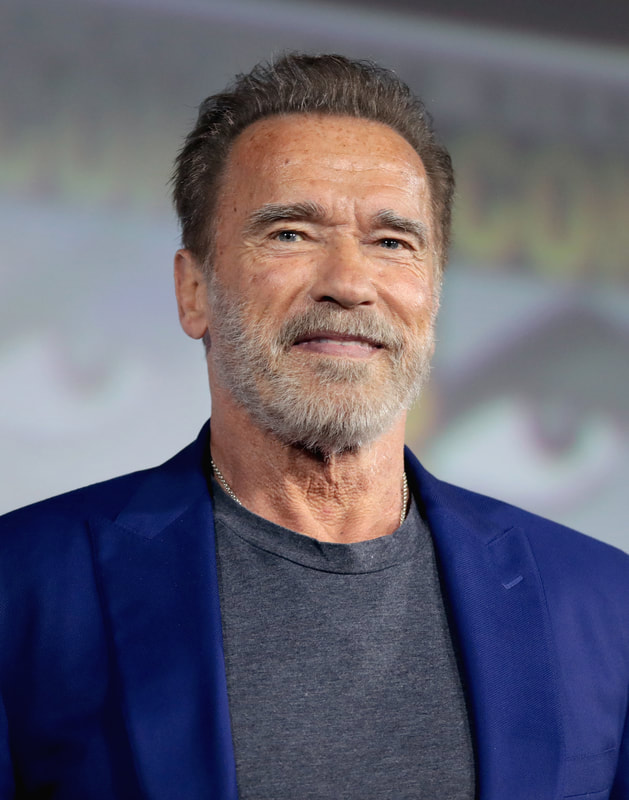

10. Bull markets are more fun than bear markets! While making money in a down market can be done, bull markets are much more forgiving. Who can argue this? Conclusion Over Farrell’s 45-year career at Merrill Lynch, he saw bull markets, bear markets, and everything in between. While investors can educate themselves by reading books or attending seminars, nothing beats decades of seat time. Through his successful and deep experience, Farrell’s rules challenge investors to study history, the madness of crowds, and their inherent “humanness” and emotions. Arnold Schwarzenegger evokes strong imagery. Big man (seven-time Mr. Olympia, five-time Mr. Universe). Big actor (Conan the Barbarian, The Terminator). Big politician (California’s governor from 2003 to 2010).

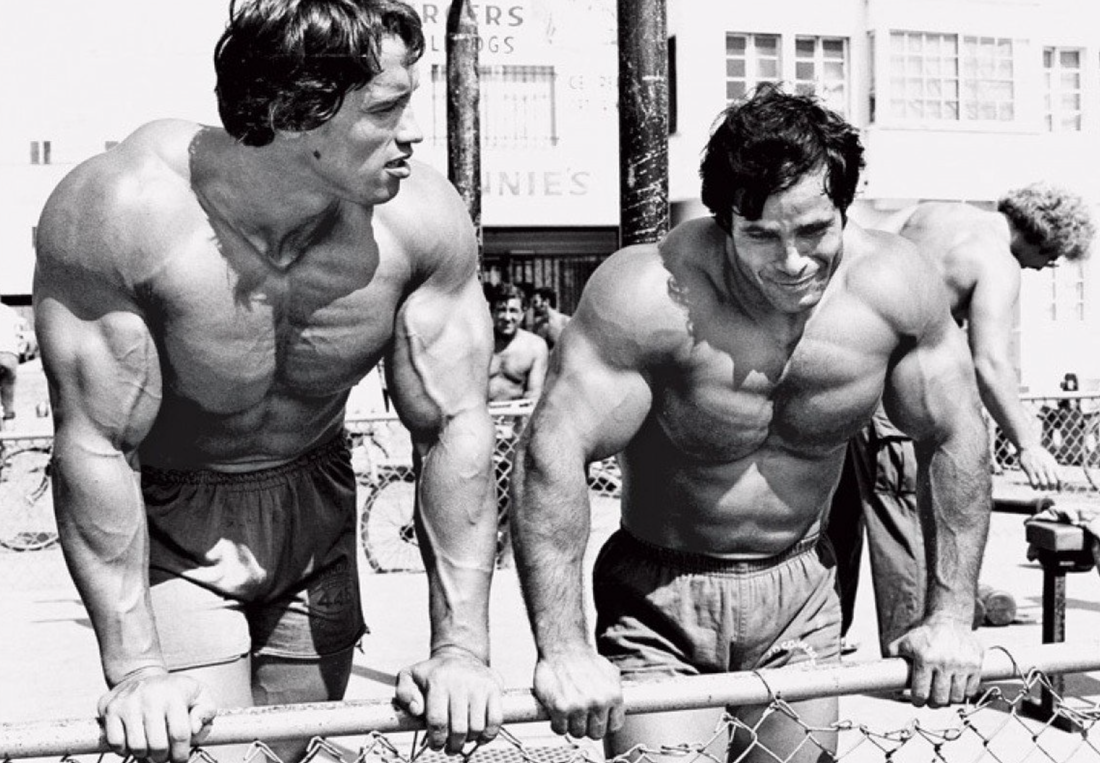

Not just physically. He was street smart, a quick learner, and intensely ambitious. Now, with an estimated network of $400 to $450 million, he’s written a book Be Useful: Seven Tools for Life, in which he looks back on is life and extols the virtues of grinding hard work and a never-say-die attitude that led to fame, fortune and, tremendous personal achievement. Now, at 76, it’s time to give back. Arnold says he wrote his new book to help people, no matter where they live in the world to become more successful. And real estate investing is at its core. He wants to dispel the most common fears that hold us back – fear of failure, choosing small goals instead of big ones, listening to all the naysayers who crush our dreams before they even start – and project positivity. He says he could have included 15 rules, but his publisher would only permit 260 pages and so he distilled his home truths into just seven. Becoming Arnie Arnie was a bodybuilding icon in the 1960s and 70’s but he had no money. Bodybuilders couldn’t making a living from their physical accomplishments in those days. You were admired within the bodybuilding community, but viewed as somewhat of a musclebound curiosity by everyone else. The one thing Schwarzenegger was not afraid of though was work. He grew up in poverty in post-World War Two Austria (born 1947) and built himself up physically, perhaps in response to beatings from his violent father. He describes himself as rebellious and refused to let domestic violence form hus father quell his spirit. He wanted to become someone. He wanted to be rich. And so, before the term side-hustle had even been thought of, Schwarzenegger began exploring ways to make money. Arnie was a bodybuilding icon in the 1960s and 70s but he had no money. Bodybuilders couldn’t making a living from their physical accomplishments in those days. You were admired within the bodybuilding community, but viewed as somewhat of a musclebound curiosity by everyone else. The one thing Schwarzenegger was not afraid of though was work. He grew up in poverty in post-World War Two Austria (born 1947) and built himself up physically, perhaps in response to beatings from his violent father. He describes himself as rebellious and refused to let domestic violence form his father quell his spirit. He wanted to become someone. He wanted to be rich. And so, before the term side-hustle had been tinvented, Schwarzenegger began exploring ways to make money.  Posing in 1966 PHOTO: HULTON ARCHIVE/GETTY One of his earliest friends was fellow bodybuilder, Mr. Olympia, and future chiropractor Franco Colombu. They worked out together, stayed lifelong friends until Franco’s passing in 2019, and were early business partners.

According to Arnie, in 1971: “I said to Frank you're a masonry worker, a bricklayer. Why don't we start a bricklaying business? I said, here in America they love this European bullshit. So, we called it Italian Masonry Expert and put a little ad in the LA Times.” As luck would have it, LA was hit by an earthquake the very next day chimneys, patios, and masonry across the sprawling city began to fall. “So, Frank and I started going out and doing estimates. Of course, we weren’t really experienced in all that stuff so we just started measuring stuff and then we always had arguments. I was always the good guy. He was the bad Italian who always charges too much. And I would say, ‘This is outrageous Frank. You cannot charge $7,600 for this. We can do it cheaper than that. No, no, no… And then he started in German, and Italian, and we started arguing. Once the theatre was over, Schwarzenegger would tell the owner he had beaten down Frank’s price to something reasonable - $5,000 – and there would be hugs all round from the home owner. Arnie says he learned these tactics while working as a sales apprentice back in Austria when he was a teenager. Instead of grooming himself for university, he worked from the age of 15 to 18 as a sales apprentice. His motto was, sell, sell, sell and this became the one of one of his Seven Rules in the new book.  “The art of selling in this case was, when I go to a customer and he says, ‘Can you tell me how much it costs to redo this chimney?’, it sounds better if you go with how you do it in a store, ‘50% off’. But of course, first they add the 50% and then take it off.” “So, my idea was, I measured it out and I said, ‘Frank, by the time we buy the material, which will be $2,000, our workmanship, it would take us a week to do this, a thousand-500 dollars each, that’s three thousand, so that’s five-thousand dollars. Frank said, ‘Five thousand, we can do it.’ Then I would go to the guy and say, ‘He wants $7,800”, and the guy would freak out. ‘Oh my god, I don't know if I can afford this. This is outrageous!’. And I would say, ‘Let me work on it.’ And so I would go to Frank and all of a sudden we would have a screaming match. And then the next thing, I go back to this guy and say, ‘I brought him down to $5,000.” And the guy would say, “Thank God!’ and he would hug me and we would get the job. So, we gave them a good deal, but we also sold them on the idea they got a special, SPECIAL deal.” Arnold was then the cement mixing brawn and Colombo was the guy who laid the bricks. Schwarzenegger drove his car to the local tool rental shop, picked up a concrete mixer, and drove it back to the site. Of course, every client noticed how jacked the two men were but the pair didn't want to reveal they couldn’t make a living from bodybuilding. So, Arnold devised a story that he had lost a Mr. Universe title in Florida because he wasn’t sufficiently tanned, which was partly true. (The other reason he says was because he was ‘a little bit too chubby”.) For the customer though, he embellished the story by swearing he would never lose a title that way again. Laying bricks a few hours every day was his way to solve the tanning problem because it allowed him to rip off his shirt and get bronzed by working in the blazing California sun. And of course, Frank was a master mason who’d worked everywhere in Italy, including helping to build the Vatican. Breaking into Movies & Commercial Real EstateArnold attributes hard work for his success. He built his body lifting weights daily. He went to America with nothing. He got on the Merv Griffin show because of his physique where Lucille Ball saw him and phoned him up him out of the blue to read for a minor role as a masseur. Schwarzenegger didn’t know much English, he had a thick Germanic accent, and he’d never acted. But he’s a Yes-and …” kind of guy with a ‘take action’ personality. “I learned the language quickly. I remember I went to Santa Monica City College and took English classes, then eventually took business classes, and all the stuff I learned as an apprentice - selling, marketing, publicity, and accounting, mathematics, micro and macro-economics, and all this stuff.

Arnie dreamed of being a leading man like Clint Eastwood, Charles Bronson and Marlon Brando – because they were all earning more than a million dollars per movie in the early 1970s. But he soon learned that life changing wealth can be generated in other days. “There was an apartment building for sale for $240,000. And I needed $37,000 for the down payment. I had in my bank account $27. So I went to Joe Weider, who was the publisher of the body building magazines, and I said, ‘can you go and loan me $10,000 for one year?’ And he said, absolutely. And so, I bought this building. Two years later, someone comes to me and offers me $500,000 for the same building. This is how much real estate went up in the 70s because of the high inflation rare. So, I immediately sold this building, took the profit and traded up to a 12-unit apartment building. Then I sold that two years later and traded up to a 36-unit building. So, in the 70s I was already a millionaire.” This post has borrowed liberally from Dana Carvey and David Spade’s podcast Fly on the Wall when the two stand up comedians interviewed Arnold Schwarzenegger. The episode was published October 25, 2023. Please listen to it – nothing replaces hearing Arnold talking. And read Arnold Schwarzenegger’s book, Be Useful: Seven Tools for Life. The building where Carvey and Spade recorded their interview was actually built by Schwarzenegger in 1984 and is now worth a small fortune compared to what he paid. https://shows.cadence13.com/podcast/fly-on-the-wall https://tim.blog/tim-ferriss-books/#tools-of-titans

One of the biggest limitations for newcomers to real estate investing is the accredited investor rule. Accredited investors don’t qualify by virtue of their specialist knowledge about investing, finance, or business. In fact, they don't need any of the above. The rule is solely based on wealth and income. If you have a lot of either, you are permitted to invest in private securities like syndicated mortgages, partnerships, and a joint ventures. If you don’t, these investment opportunities are officially prohibited. So, what’s a Private Security?

A private security is one that’s not sold on a public stock exchange like the TSX in Canada), and the NASDAQ and New York Stock Exchange in the U.S.. Air Canada, Royal Bank and Tim Hortons are random examples of public companies whose shares you can buy on the TSX. Each must abide by the rules of a publicly listed company, which include using common accounting standards, producing financial results four times a year, and holding shareholder meetings. Publicly-traded companies are meant to be transparent and rules-driven so that investors can make decisions about which of them they would like to invest in. The drive to create open information about the financial performance of public companies began after the cataclysmic crash of the US stock market in 1929 which sparked general economic collapse and The Great Depression. The stock market crashed because there were no rules preventing companies from being honest about the strength of their businesses. Many listed companies were bogus and had little or no revenue. People who bought their shares didn’t know these companies were scams, because there was no way to find out. There is a parallel here to many crypto coins. As the economy softened in the late 1920s, weak companies went bust and every other publicly listed corporation – even the financially strong ones – were dragged down with them in an explosive and destructive freefall. This is similar to the subprime mortgage crisis in 2008 when assets across the board got caught up in the downdraft caused by all the U.S. mortgage loans that were defaulting. Borrowers were defaulting because they never had the creditworthiness to be given a mortgage in the first place. Lending standards by American financial institutions leading up to 2008 were criminally lax. Back to 1929 & The Great Depression To prevent a repeat of the 1929 collapse of the stock market, the Securities and Exchange Commission (SEC) was created. Its mandate was to police publicly-listed companies by setting standards of disclosure and organizational certitude so that those investing them would feel secure in knowing their claims about revenue and expenses were accurate. Of course, if it had been doing its job, the 2008 subprime mortgage crisis would never have happened. Nor would the Bernie Madoff Ponzi scheme. So, let's just say, the SEC tries to regulate U.S. public markets. Back to being an accredited investor If you are investing in real estate joint ventures and partnerships, you must be an accredited investor if you are not wealthy or have a large income. So, how wealthy and how large? Unlike the United States, where the SEC oversees all publicly listed exchanges, Canada does not have a national body that enforces securities law. We have provincial bodies and they often don’t collaborate. There have been many examples of fraudsters scamming investors in one province only to move somewhere else and do it all over again and the provincial oversight body had no idea they were dealing with a serial offender. The federal government has come close to creating a national investor protection body but some provinces refuse to give up their provincial powers and want to keep the status quo. This issue has dragged on for years and has proved an impossible nut to crack. British Columbia’s Securities Commission defines accredited investors the following way:

In short, to be an accredited investor, you must be either wealthy or have a large income. When doing private real estate deals, the BC Securities Commission also sets standards for what it terms ‘unfair practices’:

Serious stuff. And fair enough too. These rules exist to protect investors because private securities (like real estate deals) by unregistered dealers are opaque investments and their risk level is hard to determine because the issuer (the person offering the JV or partnership) does not need to provide an offering memorandum or abide by any of the other disclosure rules that publicly-traded companies are required to. This lack of transparency makes private securities high-risk investments. But their opaque and niche nature also makes them some of the most lucrative opportunities you will ever find. Trust is key. Well-constructed contracts that protect the rights of all signatories are essential. But I’ve met scammers who would sign any contract put in front of them knowing full well that they never plan to honour the terms. In addition to well-constructed contracts, you need business partners to have honest intent and to be honorable people in their personal and professional dealings. I have a Major Problem with how Securities Law Determines Accredited Investor Status I’m not a fan of how accredited investors are defined. What’s meant to protect unsophisticated investors from putting money into ventures they don’t understand harms them in other ways. In practice, this securities law creates regulatory capture. It helps rich people to get richer and blocks those aspiring to create wealth from accessing lucrative business deals. There is no correlation between the amount of money someone possesses and their financial sophistication. What accredited investor rules really mean is that you are permitted to invest in private business deals because you already have a lot of money and it won’t hurt too much if you lose some of it. I know many people who are financially literate but prohibited from buying private securities. The only exception for unaccredited investors is if the deal they are being offered comes from “a family member, friend or close business associate”. These are private securities exceptions in British Columbia and many other jurisdictions. In other words, unless my best buddy, my sister, or a close associate at work is offering an unaccredited investor a real estate investment deal, they can’t take part. But if they have a well-paying job or a lots of cash, have at it! That could be about to change. Maybe. A glimmer of hope exists. And it’s coming from south of the border. The United States led the way in investor protection by creating the SEC in the 1930s. Now a (gentle) push is underway to redefine what an accredited investor is. In the U.S., only people with $200,000 or more in annual income or $1 million in net worth, excluding the value of their home, are accredited investors. In a rare example of bipartisanship, two bills have passed through the U.S. House of Representatives that seek to remove the wealth-exclusiveness of the accredited investor club. One bill called the Fair Investment Opportunities for Professional Experts Act recommends that those with certain licences and job experience should be accredited. This would likely include investment advisors, brokers, and ither professions. Here is the exact wording: ‘any natural person the Commission determines, by regulation, to have demonstrable education or job experience to qualify such person as having professional knowledge of a subject related to a particular investment, and whose education or job experience is verified by the Financial Industry Regulatory Authority or an equivalent self-regulatory organization (as defined in section 3(a)(26) of the Securities Ex- change Act of 1934)’ You can see the full Fair Investment Opportunities for Professional Experts Act here: https://docs.house.gov/billsthisweek/20230605/H835_SUS_xml.pdf The other bill to pass the House in June 2023 was the Accredited Investor Definition Review Act. Its intent is similar to the above Fair Investment Opportunities for Professional Experts Act, so I don’t know why we need two bills to be launched that are trying to achieve the same outcome. But both received bipartisan support and were approved by voice votes. The second bill worded its request this way: ‘an individual holding such certifications, designations, or credentials as the Commission determines necessary or appropriate in the public interest or for the protection of investors’ The full bill can be found here: https://docs.house.gov/billsthisweek/20230605/H1579_SUS_xml.pdf These two bills have moved to the Senate and it’s anyone’s guess if they will be supported there. There is very little Democrats and Republicans agree upon, and even if they do, U.S politicians usually find ways to nullify bipartisan agreement through tribal beliefs and blood feud allegiances that are kindly referred to as differences in ideology. Really, it’s a cut-off-my-nose-to-spite-my -face parochialism. It’s the Hatfields versus McCoys: if they propose it, I’ll oppose it, even if I agree with them. Nonetheless, we should be glad a conversation has started about what it means to be an accredited investor. This conversation, as tepid as it is, is important because if changes are made in the U.S., similar legislation could be proposed here in Canada. Canada is a more difficult jurisdiction to achieve change however. The absence of a national markets regulator like the SEC means investor laws would have to be changed province by province. But if the U.S. changes to its accredited investor rules, so should we. In fact, why wait. Canada, do it now! Those with financial acumen should be allowed to invest in private securities, no matter their level of wealth. A Much Better Solution The two American bills currently under consideration ask for people who possess certain licences and professional designations to be accredited. That is still discriminatory. The best answer would be creating an accredited investor curriculum. Anyone could study the curriculum and take an exam. Pass it and you would be an accredited investor, no matter your age, gender, or socio-economic status. This would be fairer. It would open up new investment opportunities for the educated who would now have the certified skills to assess the risk of their investments. And it would create a larger pool of money that could be invested in private real estate deals, start-ups, and other entrepreneurial endeavours. Win-win. |